Signed into law in 2025, the “One Big Beautiful Bill” (OBBB) introduces a range of changes that could impact retirees. Whether you’re already enjoying retirement or planning for it soon, understanding these legislative changes can help you evaluate your financial plan in light of both potential benefits and considerations.

In this guide, we’ll walk through the bill’s key points to help you understand how these changes may affect your retirement planning.

Signed into law in 2025, the “One Big Beautiful Bill” (OBBB) introduces a range of changes that could impact retirees. Whether you’re already enjoying retirement or planning for it soon, understanding these legislative changes can help you evaluate your financial plan in light of both potential benefits and considerations.

In this guide, we’ll walk through the bill’s key points to help you understand how these changes may affect your retirement planning.

Table sources: 1, 2, 3, 4

The information provided here is a general summary of key provisions from the One Big Beautiful Bill and is for informational purposes only. Individual eligibility for tax deductions or exemptions depends on your personal financial situation and may be subject to limitations, income thresholds, or future legislative changes. This summary does not constitute tax or financial advice. Please consult your tax advisor or financial professional to evaluate how these provisions may apply to your specific circumstances.

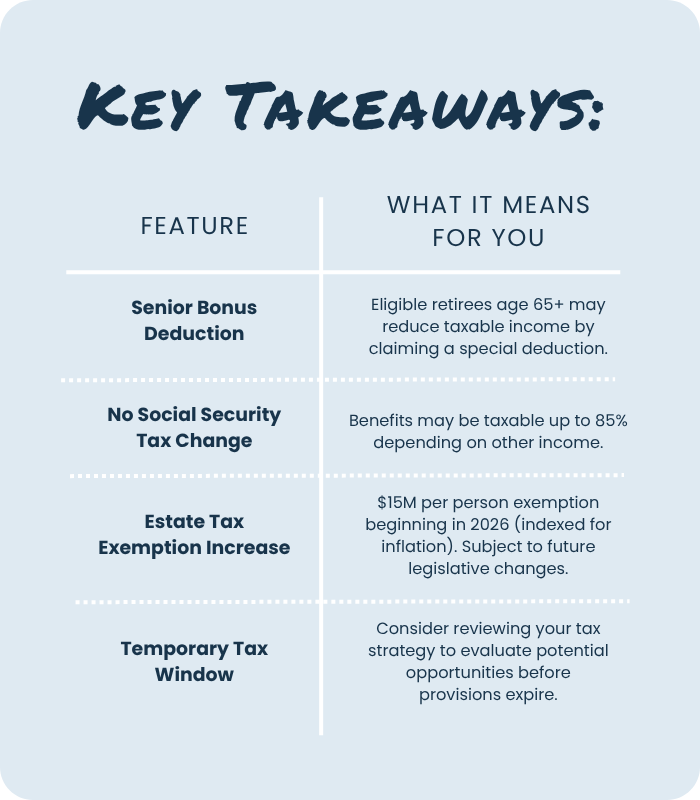

The New “Senior Bonus Deduction”

The Big Beautiful Bill introduces the Senior Bonus Deduction, a special tax provision targeted specifically to retirees.

So, what exactly is it? Starting in 2026, individuals aged 65 and older may be eligible to claim this additional deduction on their federal income taxes. The deduction reduces taxable income by $6,000 for individuals, or $12,000 for married couples filing jointly. This provision applies for tax years 2026, 2027, and 2028.1

Why does this matter? For many retirees, income in retirement may come from a mix of Social Security benefits, retirement account withdrawals, and possibly part-time work. This deduction may help reduce the taxable portion of your retirement income, depending on your specific income sources and tax situation. By lowering taxable income, eligible retirees could owe less in federal taxes during retirement.

No Changes to How Social Security Is Taxed

Despite some expectations, the Big Beautiful Bill does not change how your Social Security benefits are taxed. Up to 85% of your Social Security benefits may still be taxable, depending on your other sources of income.2

Why does this matter? Many retirees hoped for relief from these taxes, but for now, it’s important to be aware of how other income sources can impact the taxation of these benefits.

Estate Planning Just Got More Flexible

If you’re thinking about legacy planning, the bill introduces a key update. Beginning in 2026, the law increases the federal estate, gift, and generation‑skipping transfer tax exemption to $15 million per person, or $30 million for married couples filing jointly (indexed for inflation).3

Why does this matter? A higher exemption amount may offer greater capacity for transferring assets through inheritance, gifts, or trusts without triggering federal estate taxes, depending on their individual estate size and financial situation.

Because the exemption is indexed for inflation and not currently set to expire, there’s no scheduled deadline requiring immediate action. However, like all tax laws, this provision could be changed through future legislation. 4

Potential Risks: Medicaid and Food Assistance

While the Big Beautiful Bill includes several tax benefits, it also reduces funding for key safety-net programs, which could impact access to healthcare and support services for some retirees.

Starting in 2026, the law calls for Medicaid cuts, which the Congressional Budget Office estimates amount to nearly $1 trillion over the next decade.1 These changes include:

Required Minimum Distributions (RMDs) Get Trickier—Not Easier

While many retirees were hoping for more flexibility around Required Minimum Distributions (RMDs), the Big Beautiful Bill doesn’t deliver on that front. As of now, the RMD start age remains on the gradual path set by the SECURE 2.0 Act, which moves the starting point from age 73 to age 75 over the coming years. No further changes were made in the Big Beautiful Bill.

But what’s raising concern for financial planners is a new provision requiring the U.S. Treasury Department to study the imposition of RMDs on Roth IRAs and large 401(k) balances. While no changes have been made, this study suggests that future policy decisions may consider whether tax-deferred or tax-free accounts, such as Roth IRAs, could be subject to mandatory withdrawals.1

Why Proactive Planning Matters

Many provisions of the Big Beautiful Bill, including the Senior Bonus Deduction, are temporary, scheduled to end in 2028. This makes the years between 2026 and 2028 especially important for planning.

Reviewing your financial situation during this period may help you determine how these temporary provisions affect your personal strategy.

Topics to consider reviewing with a financial or tax professional:

Although some of these strategies can seem complex, you don’t need to navigate them alone. Working with a qualified financial or tax professional may help you evaluate how the Big Beautiful Bill’s provisions relate to your personal situation.

Sources

Disclosures:

Investment Advisory Services offered through Trek Financial LLC, an investment adviser registered with the Securities Exchange Commission. Information presented is for educational purposes only. It should not be considered specific investment advice, does not take into consideration your specific situation, and does not intend to make an offer or solicitation for the sale or purchase of any securities or investment strategies. Investments involve risk and are not guaranteed, and past performance is no guarantee of future results. For specific tax advice on any strategy, consult with a qualified tax professional before implementing any strategy discussed herein.

The information provided here is a general summary of key provisions from the One Big Beautiful Bill and is for informational purposes only. Individual eligibility for tax deductions or exemptions depends on your personal financial situation and may be subject to limitations, income thresholds, or future legislative changes. This summary does not constitute tax or financial advice. Please consult your tax advisor or financial professional to evaluate how these provisions may apply to your specific circumstances.

The potential financial impact of these provisions depends on individual circumstances. No outcome is guaranteed. Tax laws and regulations are subject to change, and provisions of the Big Beautiful Bill may be amended or repealed by future legislation. Information is based on publicly available legislative summaries and independent third-party sources, including Congressional Budget Office estimates. Trek 25-265